Download slides

Download slides

Diesel volatility emerges as strategic risk for trucking

Published: Thursday, April 09, 2026 | 09:00 am CDT

Fuel volatility remains a key watch item for shippers

As the conflict involving Iran stretches into its second month, energy markets are shifting from reacting to headline risk to pricing in persistence. Ongoing military activity continues to inject a structural risk premium into global oil markets, particularly around maritime security and insurance costs.

The key questions have evolved from if disruption will occur to how sustained interruptions may become—and whether mitigation measures can keep pace over time. The Strait of Hormuz remains the critical swing factor, with even short-lived disruptions or escalations reinforcing volatility and keeping fuel markets on alert.

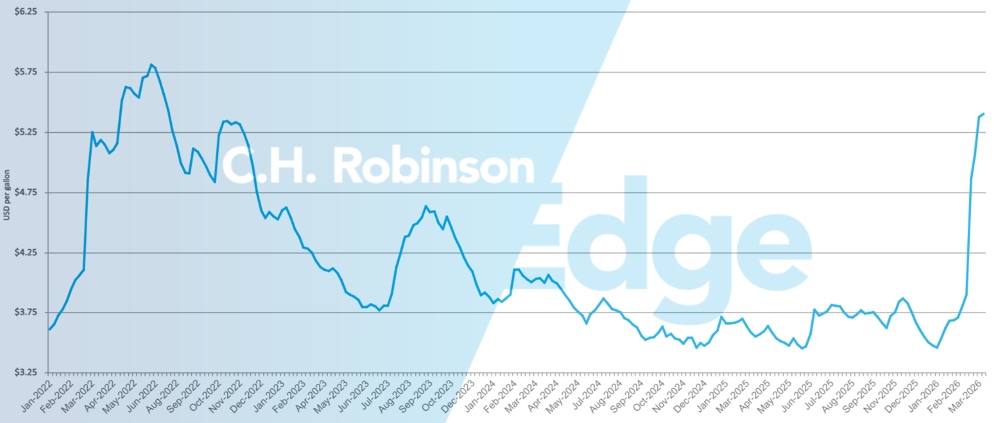

In the United States, higher diesel matters because fuel remains one of the largest operating inputs for trucking. According to ATRI benchmarking, fuel represented roughly 21% of total cost per mile in 2024 and exceeded 28% of costs during prior fuel spikes. The national U.S. average diesel price per gallon in early April was $5.65, up from the March average of $4.92 and $3.72 in February.

While fuel is largely treated as a passthrough, periods of rapid volatility have a bottom-line impact on carriers who absorb exposure through deadhead, empty repositioning, and timing gaps in fuel surcharge mechanisms. Historically, sustained diesel volatility has intensified pressure on carrier margins, accelerated capacity exits, and reshaped market share.

Fuel dynamics are also influencing global transportation. For ocean carriers, bunker fuel can represent up to 60% of voyage costs, and diversions around conflict zones lengthen routes and raise fuel consumption. Air carriers face similar pressures when avoiding restricted airspace, increasing burn and surcharge risk.

Looking ahead, shippers should treat fuel as a strategic risk variable, not just a line item. Refining lane strategies, diversifying capacity mixes, stress testing fuel surcharge assumptions, and maintaining flexibility in routing and mode selection will be critical as fuel volatility continues to challenge budget predictability in the months ahead.

The national U.S. average diesel price per gallon of $4.92 in March was up from $3.72 in February. Fuel prices have increased each week of the month and started April at over $5.65. The surge in diesel prices has pushed the per gallon rate to levels not seen since mid-year 2022. As evident in the charts below, fuel has been relatively stable at low levels for years.

Now with a rapid surge in fuel pricing, shipper budgets are being constrained, leading to questions about what can be done to mitigate these rising costs. With fuel surcharges in the spotlight, C.H. Robinson has prepared this white paper to provide a better understanding of truckload fuel surcharges.

U.S. average diesel price per gallon

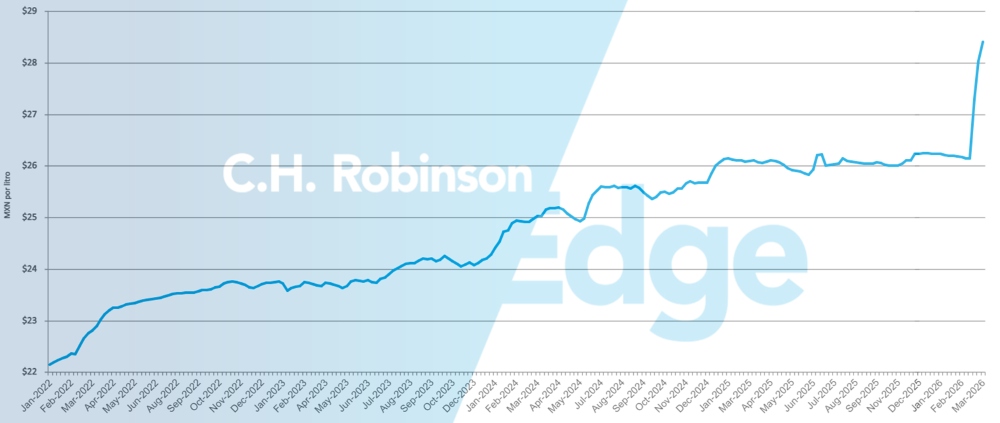

The Mexico average diesel price per liter of fuel has increased approximately 9% over the past month, and due to the previous stability of diesel pricing, is up about the same 9% over the past year. While this is the largest increase in diesel pricing that Mexico has seen in years, the 9% increase is rather tame compared to other countries such as the United States who have seen pricing increases over 40% since the conflict in Iran began.

Mexico average diesel price per gallon

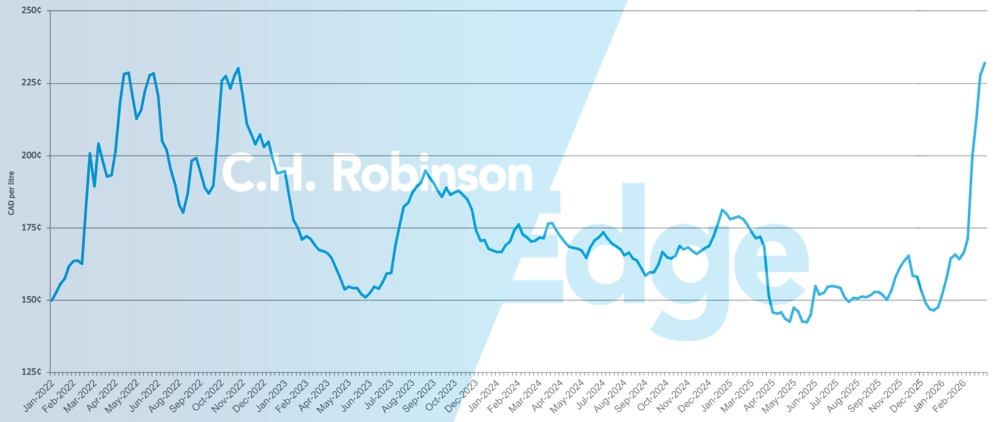

The national average diesel price in Canada, shown here in Canadian cents per liter, has increased significantly in recent weeks.

Canada average diesel price per gallon

Actionable freight insights

Actionable freight insights