Download slides

Download slides

Port stability holds as inland variability emerges

Published: Thursday, April 09, 2026 | 09:00 AM CDT

Onthispage

Stability holds at the port level, but variability is shifting inland

North American ports enter April in a largely fluid position, with most major U.S. gateways operating below peak capacity. Seattle‒Tacoma terminals are running near 55‒60% utilization, while New York‒New Jersey is closer to 65%, indicating available throughput across both coasts.

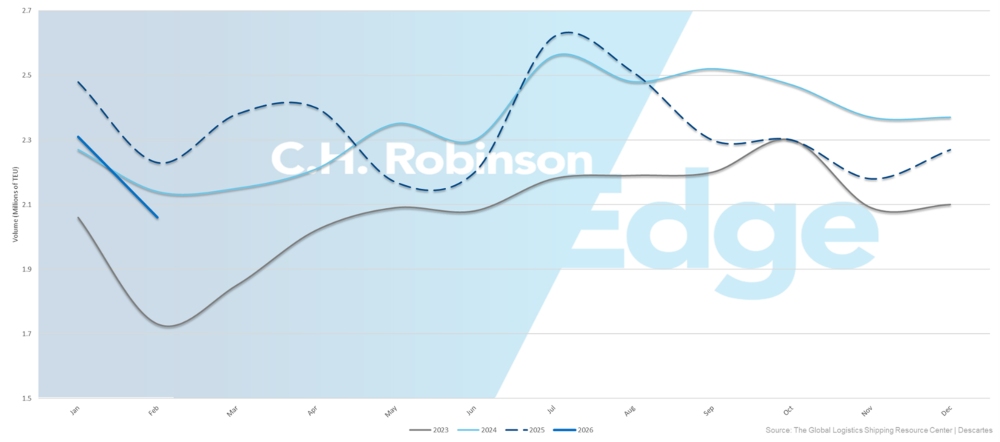

U.S. container imports declined in February but remained in line with post-pandemic averages, suggesting that overall volume levels continue to support stable port operations. While demand has moderated from prior peaks, throughput remains balanced contributing to fluid conditions at the terminal level.

U.S. container import volumes

This relative stability at the port level is masking a more nuanced operating environment inland, where rail performance, equipment availability, and localized disruptions are shaping execution outcomes. While headline congestion remains limited, variability is increasingly occurring beyond the terminal gate—requiring closer coordination across drayage and intermodal networks.

Seasonal rail constraints continue to influence inland performance

Lingering winter conditions continue to affect inland network fluidity, particularly across Canada. Rail providers are still operating under seasonal protocols in some regions, including reduced train lengths and speed restrictions, which are limiting capacity and extending transit times. Halifax experienced dwell times reaching up to 15 days in March following vessel bunching and late-winter storms, though conditions have since improved.

In the United States, inland hubs remain sensitive to volume shifts. Chicago’s Norfolk Southern (NS) Landers ramp stabilized near 48-hour dwell by late March, but performance remains dependent on weather and throughput consistency. Cincinnati, by contrast, saw improved fluidity after a carrier shifted volumes from NS Sharonville to a nearby CSX facility, easing chassis constraints and improving turn times. These dynamics suggest inland performance is stabilizing overall—but remains highly dependent on lane-specific conditions.

Drayage networks adjust to rising costs and regulatory signals

Drayage networks are entering a period of adjustment as cost pressures and regulatory developments converge. Diesel prices rose through March—reaching their highest levels since late 2022—increasing operating costs across the trucking sector and placing pressure on smaller carriers. Some providers are responding by reducing coverage or adjusting rate structures, which is contributing to tighter capacity in select markets.

In parallel, new regulatory proposals aimed at tightening licensing standards for non-domiciled drivers could gradually reduce the available driver pool over time. While the full impact is expected to materialize over several years, early signals suggest carriers are already evaluating network exposure. Together, these dynamics point to a drayage market that remains functional but is becoming more selective and cost sensitive. Shippers may begin to see greater variability in pricing and service consistency across regions.

Shifting cargo flows introduce new regional pressure points

Changes in global routing patterns are beginning to influence port dynamics. Disruptions in the Middle East and reduced Suez Canal transits are prompting some importers to redirect cargo toward United States West Coast (USWC) gateways. While these ports are currently operating with available capacity, even modest volume increases could begin to tighten drayage, chassis availability, and inland connections—particularly given the capacity reductions seen in recent years.

Meanwhile, certain areas are experiencing localized congestion. Jacksonville, Florida is experiencing elevated dwell and extended truck turn times due to gate constraints and high yard utilization, highlighting how quickly conditions can diverge at the port level. Overall, while the broader network appears balanced, localized surges and infrastructure limitations continue to create uneven operating conditions.

Stable networks with narrower margins for error

Overall, the ports and drayage landscape remains operationally sound, but the margin for disruption is narrowing. While port congestion remains limited, inland and drayage variability is having a greater impact on execution.

Looking ahead, shippers may benefit from focusing less on port-level conditions and more on end-to-end network performance—particularly inland rail reliability, equipment positioning, and drayage partner capacity. In an environment where the macro picture appears stable, it is increasingly the micro-level shifts that will determine service outcomes.

Planning ahead

- Account for seasonal inland variability: Build additional lead time into shipments moving through Canadian gateways and inland rail networks as seasonal constraints ease unevenly.

- Monitor shifting cargo flows: Track early indicators of volume changes at USWC ports as routing patterns adjust and prepare for localized capacity tightening.

- Secure drayage capacity proactively: Strengthen relationships with core providers and align on expectations as cost pressures and regulatory signals evolve.

- Incorporate equipment planning into execution: Actively manage chassis availability, container positioning, and street-turn opportunities to reduce delays.

Notable shifts this month

USWC volumes show early signs of rebalancing

Trans-Pacific volumes into the USWC are beginning to show a modest recovery after prolonged diversion to U.S. East and Gulf Coast ports. Ongoing disruptions in the Middle East and reduced Suez Canal transits are prompting some shippers to reconsider all-water routings, shifting select volumes back to Los Angeles/Long Beach and Pacific Northwest gateways. While overall volumes remain below historical peaks, early indicators suggest a gradual uptick into Q2.

Current port operations remain fluid, meaning the impact is not yet visible in congestion metrics. However, even incremental volume increases can begin to tighten drayage capacity, chassis supply, and warehouse availability in key markets. If this rebalancing continues, localized constraints could emerge quickly, particularly in regions where capacity scaled down over the past two years.

Jacksonville congestion intensifies despite broader stability

Port conditions across the United States southeast remain generally stable, but Jacksonville is emerging as an outlier as congestion persists into early April. Truck turn times are averaging 3‒4 hours, driven by gate limitations, high yard utilization, and constrained landside infrastructure. With most containerized traffic concentrated at a single terminal, the port has limited flexibility to absorb surges.

Conditions are not easing at the same pace as other U.S. gateways, suggesting congestion may persist in the near term. Terminal operators are implementing mitigation measures, including adjusted gate operations and backlog-clearing strategies, though improvement may be gradual. For shippers, this highlights the need to monitor port-specific conditions and maintain flexibility in drayage and inland planning.

Seasonal transition introduces new variability in Canadian networks

Canadian rail and inland networks are entering a transitional phase as winter operating conditions begin to ease, but network performance remains uneven. While some restrictions—such as reduced train lengths and speed limits—are gradually lifting, residual imbalances in equipment and railcar positioning continue to affect capacity and transit consistency. Halifax dwell times peaked at 14‒15 days in late March following vessel bunching and weather disruptions, and although fluidity has improved, recovery across the network is not uniform.

The shift into spring introduces new constraints, including thaw-related weight restrictions on trucking routes that can limit inland flexibility. These overlapping factors suggest that variability may persist even as winter pressures recede. For shippers, this transition period may require additional planning buffers and closer coordination across intermodal handoffs to maintain reliability.

Key takeaways

- Stable ports do not eliminate execution risk: Inland rail performance and drayage capacity are becoming more influential in determining shipment outcomes.

- Early USWC volume shifts may tighten local capacity: Even modest demand increases can impact chassis, drayage, and warehouse availability.

- Drayage conditions are becoming more selective: Cost pressures and regulatory signals may reduce flexibility in certain markets over time.

- Localized disruptions remain the primary risk: Monitor specific ports, ramps, and terminals where congestion or constraints may emerge.

- Build flexibility into inland planning: Additional lead time and routing options can help mitigate variability during seasonal transitions.

Actionable freight insights

Actionable freight insights